Mixed cost

Mixed cost

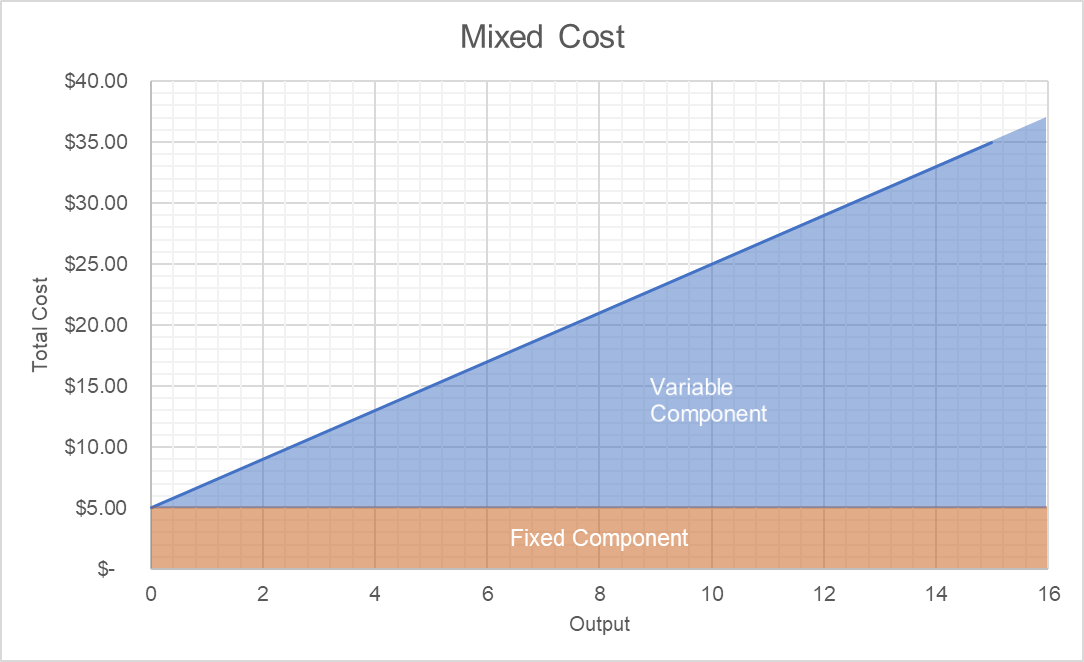

A mixed cost is a cost that contains both a fixed cost component and a variable cost component. It is important to understand the mix of these elements of a cost so that one can predict how costs will change with different levels of activity. Typically, a portion of a mixed cost may be present in the absence of all activity. In addition to which the cost may also increase as activity levels increase. As the level of usage of a mixed cost item increases, the fixed component of the cost will not change, while the variable cost component will increase.

The formula

Y = a + bx

Y = Total cost

a = Total fixed cost

b = Variable cost per unit of activity

x = Number of units of activity

Mixed costs are common in a corporation, since many departments require a certain amount of baseline fixed costs to support any activities at all, and also incur variable costs to provide varying quantities of services above the baseline level of support. Thus, the cost structure of an entire department can be said to be a mixed cost. This is also a key concern when developing budgets since some mixed costs will vary only partially with expected activity levels. Also, it must account for in the budget.

Example of a Mixed Cost

If a company owns a building, the total cost of that building in a year is a mixed cost. The depreciation associated with the asset is a fixed cost since it does not vary from year to year, while the utility expense will vary depending upon the company’s usage of the building. The fixed cost of the building is $100,000 per year, while the variable cost of utilities is $250 per occupant. If the building contains 100 occupants, then the mix cost calculation is:

$125,000 Total cost = $100,000 Fixed cost + ($250/occupant x 100 occupants)

{kind=link}